The HarvRESt Business Model Catalogue Is Out: 33 Ways European Farms Are Making Renewable Energy Pay

The new HarvRESt Business Model Catalogue maps how European farms are turning renewable energy into a business and reveals that the biggest barriers to scaling up are bureaucratic, not technological.

Across Europe, increasing numbers of farmers are exploring opportunities to diversify their income through renewable energy production. Ask why they haven't yet, and the answer is rarely about technology. Solar panels above the crops, biogas from manure, self-consumption systems that shave the electricity bill, all of which exist and work today. What's missing is everything around it: the contracts, the ownership structures, the permits, the financing. In a word, the business model. That gap is what HarvRESt's newly published Business Model Catalogue sets out to close.

What's actually in the catalogue

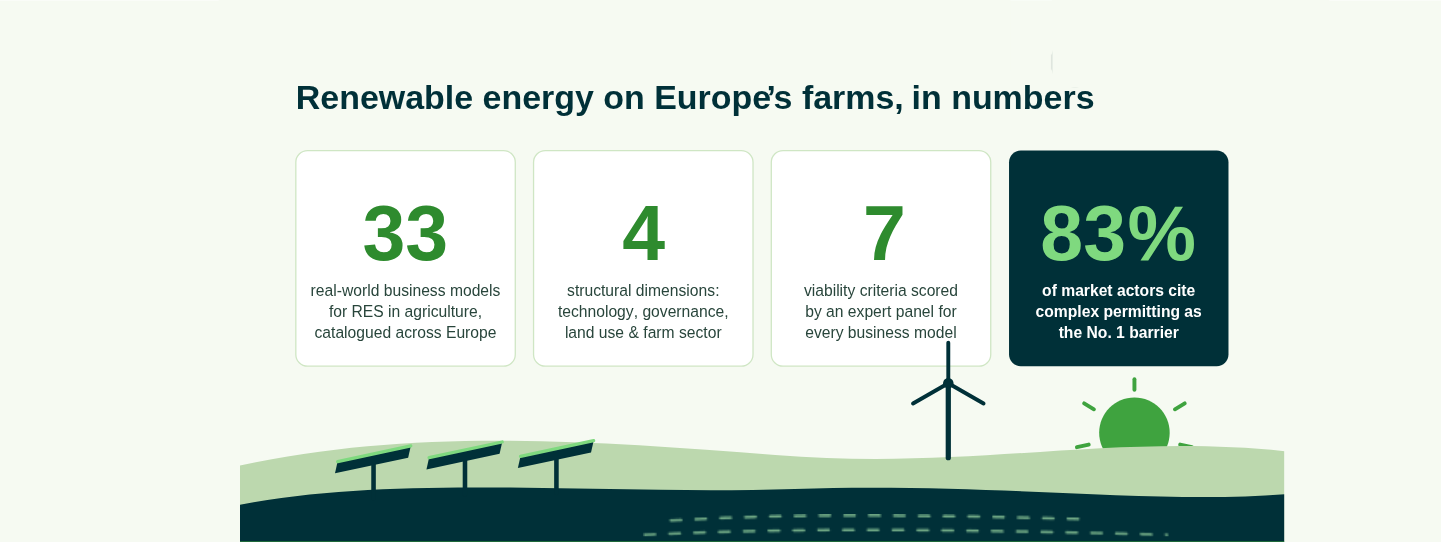

The study, led by project partner Engreen with contributions from Climate-KIC and HEC, gathers 33 business models that already operate somewhere in Europe. No two are quite alike. Some are individual farmers who own their installations outright. Others are cooperatives, or arrangements where an energy service company owns and maintains the hardware while the farmer simply hosts it. To make the collection navigable, each model is sorted along four dimensions: the technology it uses, who owns and governs it, how it treats the land, and which agricultural sector it belongs to.

An expert panel then scored every single model against seven viability criteria, among them long-term resilience, replicability across regions, sustainability and circularity, and how attractive the model looks to farmers on one side and energy companies on the other. The point was to work out which models can realistically scale, and which will remain local curiosities.

"Many of the technologies covered by the catalogue are already available. The challenge is creating the conditions that allow farmers to adopt them at scale," says Nicola Stenico, Engreen, who is one of the lead contributors to the catalogue.

Strong interest from farmers across Europe

The assessment suggests that many farmers see renewable energy as a potential additional source of income. Existing self-consumption schemes have already demonstrated that on-farm energy production can deliver tangible economic benefits.

The assessment highlighted an important trade-off between resilience and ease of adoption. Agrivoltaics and biogas score best on circularity and long-term resilience, but they are expensive to set up and complicated to run. Standalone solar and third-party leasing are the opposite: cheap to enter, quick to scale, less impressive on paper. For a farm or a region taking its first steps into energy, that makes them the obvious place to start.

Regulatory and administrative barriers remain significant

When the project asked market actors what holds agricultural energy back, 83% pointed to the same thing: permitting. The issue was not technology costs or equipment availability, but administrative procedures. Nearly half of respondents also admitted they simply don't know which subsidies they qualify for, or which rural governance rules apply to them.

Two structural problems make it worse. Private investors decide in weeks; public administrations decide in years. Put the two in the same project and the partnership tends to stall before it starts. Meanwhile, in several European regions, grid rules still forbid neighbour farms from trading electricity with each other, which locks farmers into isolated self-consumption when they could be forming interconnected agro-energy communities.

And the barriers look very different depending on where you stand. In Spain, solar and biogas are already widespread; the question there is grid integration, not installation, though permitting frustration runs high. In the Italian cases covered by the study, 60% of respondents reported no renewable technology deployment, illustrating how uneven the transition remains across Europe. Norway has strong coordination platforms and supportive municipalities, but a regional grid monopoly blocks local energy sharing. Germany, finally, offers a warning to everyone: two decades of shrinking subsidies turned agricultural biogas from a flagship technology into a stagnating one.

Implications for future deployment

The findings point to several actions that could help accelerate uptake. Where administration is slow, start with what is simple and commercially proven, farmer-owned or ESCO-managed solar, because those models don't need the bureaucracy to cooperate. The more ambitious configurations, multi-source hybrid systems and collective cooperatives, will have to wait for policy to catch up: open grids, simpler cross-sector permits.

Inside the project, the catalogue now has a job to do. Its typologies and rankings feed directly into HarvRESt's two digital tools, the Decision Support System and the Agricultural Virtual Power Plant, so that the recommendations these tools give to farmers and policymakers reflect how the market actually behaves as well as the economic and regulatory conditions faced by farmers and energy developers.